October 12th, 2017 - October 15th, 2017. 332-335 days since the Nov 8, 2016, election of some rich asshole, no.45, and 264-267 days since the Jan 20th inauguration.

FCC Rebukes the rich asshole, Refuses To Dismantle First Amendment Over His Petty Tantrums

some rich asshole has recently come under fire for his most autocratic charge yet, which is that the free press should be regulated for writing bad things about him. He even mentioned somehow getting rid of their licenses.

Jessica Rosenworcel, a commissioner for the Federal Communications Commission, says of the rich asshole’s tweets challenging the rights of the free press:

“I think it’s essential that the FCC and all that it does is careful to abide by the First Amendment when it engages in any kind of policies involving broadcast licensees.”

Rosenworcel went even further when she was questioned about the rich asshole’s suggestions that the First Amendment should somehow be impeded from the bully pulpit of the White House:

“I think it’s important to realize that the Supreme Court characterizes our First Amendment as a profound national commitment to having robust, uninhibited and wide open debate and you know, that debate can sometimes be hard hitting for public officials.”“But it is absolutely essential that we support the first amendment and everything that the FCC does.”

She went on to say that it is the duty of other FCC commissioners and employees to go public and defend the First Amendment, no matter what the rich asshole does or says. Rosenworcel made clear what she thought of what the media should do in regards to the rich asshole’s tantrums and dissatisfaction with journalists speaking truth to power:

“I think it’s important for all the commissioners to make clear that they support the First Amendment.”“And that the agency will not revoke a broadcast license simply because the president is dissatisfied with the licensees coverage.”

Hopefully others in the FCC feel the same way. some rich asshole is taking the first steps to turn America into an autocracy or a dictatorship, and we should not tolerate his antics. In fact, our resisting them could save the republic.

Mike Huckabee appears on Fox News (screen grab)

DON'T MISS STORIES. FOLLOW RAW STORY!

Former Republican presidential candidate Mike Huckabee said on Sunday that he could not recall whether President some rich asshole admitted sexually assaulting women even though the now-president was caught on a leaked Access Hollywood tape saying that he grabbed women by the “by the pussy.”

While appearing on Fox & Friends, Huckabee blasted former Democratic presidential nominee Hillary Clinton for suggesting that Russia helped the rich asshole win the election.

“There was also an uncomfortable moment when she talked about President the rich asshole, how he admitted to being sexual assaulter,” Fox News host Abby Huntsman said. “She was asked about the [Harvey Weinstein sexual assault allegations] and she mentioned how her husband has — what he did was in the past. Anyone watching that, I think, was a little squirmy in their seat.”

“Has President the rich asshole ever admitted to being a sexual assaulter?” Huntsman wondered.

“I don’t recall that that’s ever happened,” Huckabee said. “But I do recall that Bill Clinton lost his law license. He was impeached. He admitted that he lied under oath and that there had been a number of women who have never been disproven to be wrong about their allegations regarding him.”

The former Arkansas governor said that he didn’t want to “dig up” dirt on the Clintons “but she keeps bringing up how pure she and her husband were.”

Watch the video below from Fox News.

DON'T MISS STORIES. FOLLOW RAW STORY!

U.S. President some rich asshole will hurt low-income Americans by doing away with Obamacare subsidies and make it harder for him to engage in bipartisan talks with Democrats as Congress edges toward a possible government shutdown, lawmakers said on Sunday.

The White House has announced that the Republican administration will stop paying billions of dollars to insurers to help low-income consumers meet out-of-pocket medical expenses, as part of the president’s step-by-step effort to dismantle the Affordable Care Act, Democratic former President Barack Obama’s signature healthcare law.

The expected loss of cost-sharing subsidies, estimated to be worth $7 billion this year and $10 billion in 2018, has prompted worries about insurance market chaos and undermined the prices of insurer and hospital company shares.

By antagonizing Democrats who support Obamacare, the rich asshole’s actions could also lead to political turmoil over spending in December, when Republicans hope to put the final touches on a sweeping tax reform bill.

Republican Senator Susan Collins, who has opposed the rich asshole-backed legislation to repeal and replace Obamacare, warned that the president’s move will also affect the ability of vulnerable low-income people to access healthcare and afford out-of-pocket medical costs.

“I’m very concerned about what the impact is going to be for people,” Collins said on CNN’s “State of the Union”.

“The funding that is available under the cost-sharing reductions is used to subsidize their out-of-pocket costs. And if they can’t afford their deductible, then their insurance is pretty much useless.”

Asked if the rich asshole’s actions would hurt Americans, she replied: “I do believe that.”

Last week, the president also offered an invitation for Democratic leaders to come to the White House to negotiate on healthcare.

But House of Representatives Democratic leader Nancy Pelosi showed little interest on Sunday.

“We’re a little far down the road for that,” Pelosi said on ABC’s “This Week” program.

Pelosi indicated that the president’s actions and continued White House pressure to fund a wall on the U.S.-Mexico border could make it harder for Republicans to win Democratic cooperation in December, when a current government spending measure is due to expire.

“He wants to negotiate the healthcare bill by repealing the Affordable Care Act and building a wall? No,” Pelosi said.

“The Republicans have the majority. They have the signature of the president. It’s up to them to keep government open.”

Collins and Pelosi see a bipartisan path on healthcare in discussions on possible legislation between Republican Senator Lamar Alexander and Democratic Senator Patty Murray.

Republican Senator Lindsey Graham told CBS’ “Face the Nation” that the rich asshole has also encouraged Alexander to get a bipartisan deal but also wants any future healthcare bill to reform the current system.

“The president is not going to continue to throw good money after bad, give $7 billion to insurance companies unless something changes about Obamacare that would justify it,” Graham said. “It’s got to be a good deal.”

David Morgan

October 15, 2017

Tom Porter

Posted with permission from Newsweek

President Donald Trump’s decision to end a provision of the Affordable Care Act will most impact the core support that carried him to the presidency, according to new research.

Nearly 70 percent of those affected by Trump’s executive order last week ending cost-sharing reduction subsidies live in states that voted for him last November, according to new research by the Associated Press.

The White House announced on Thursday that it was stopping subsidies that were provided by the federal government to help provide medical insurance for low income Americans.

The research shows the political risk being taken by Trump in his bid to end Obamacare, with the president likely to face blame for the move which is expected to sharply increase insurance costs.

According to research cited by AP by the U.S. Centers for Medicare and Medicaid Services, the provision in the bill ended last week benefited 6 million Americans, with 4 million of them living in the 30 states Trump won in the election.

Of the 10 states that benefit most from the subsidy, all but one voted for Trump. Among those most affected will be Mississippi, Florida and Arkansas.

Some Republicans have expressed concern about the potential impact of the move at the ballot box.

“I think the president is ill-advised to take this course of action, because we, at the end of the day, will own this,” Republican Congressman Charlie Dent of Pennsylvania said Friday on CNN. “We, the Republican Party, will own this.”

Trump’s bid to fulfill his campaign promise to repeal Obamacare has come unstuck in Congress, with the White House failing to secure the support required in the GOP backed House and Senate. The president had threatened to end the subsidies before acting Thursday.

the rich asshole Voters Threw our Country Under the Bus, Now they are Having Regrets – Big Time

53 Comments

3.5 k Views

Criticize the rich asshole all you want. God knows I sure do it a lot. But criticism can’t get you that far. After all, we knew what the rich asshole was going to do. He campaigned on banning Muslims, he said the Paris Accord was a “bad deal”, he said that his “number-one priority is to dismantle the disastrous deal with Iran”, he also said he would withdraw from international trade deal TPP. Lots of the rich asshole supporters are experiencing regrets for their vote, considering the rich asshole actually enforced what he said that he would.

Take the TPP, for example. The TPP was the successor to the North American Free Trade Agreement, which, as the rich asshole pointed out during the campaign, led to outsourcing. Millions of the rich asshole supporters in the agriculture industry stood at his rallies and cheered as the rich asshole vowed to withdraw America from the TPP, if elected.

American agriculture business was plenty angry. The industry was struggling. the rich asshole convinced them, that their financial burdens were caused by those pesky TPP imposed tariffs. As a result of the TPP, the United States could not sell products to many countries.

But as the rich asshole pulled us out of the TPP, almost instantly, there were countries taking our place. Countries like Australia, Mexico and the European Union were negotiating even lower tariffs with each other. America is not invited to these parties.

The EU exports as much pork to Japan as United States does. On July 6, the EU announced a deal that would give European pork up to $2 per pound over US pork. Same with European wine. Now, a 15% tariff on European wine to Japan has been removed, Politico.

In August, many US pork farmers were shocked when sales dropped by 9%. According to the rich asshole, business was supposed to sky rocket because of lower tariffs in the TPP. Turns out the rich asshole’s business intuition is kind of shitty. the rich asshole didn’t predict other nations swooping in.

Those same farmers were the ones that carried the rich asshole to the White House. Now they realize that they had been tricked. Many of them have regrets. According to a Reuters poll, the rich asshole support has dropped in rural America from 55 last winter, to 47 a month ago.

Regrets can be tough, especially when your decision leads to losing your job, or not being able to put enough food on your families table. Regrets over voting for the rich asshole are even more brutal, considering how these voters were tricked. the rich asshole made America hate Hillary, a woman who devoted her life to helping children and women. There was a time, that the majority of Americans felt Hillary had broken several laws. It turns out that all of these “crimes” were just manufactured by the rich asshole campaign and Julian Assange. And still, she hadn’t been convicted of a single crime.

America was tricked, and now we must be punished. The world is being punished as a result of the rich asshole presidency as well. Japan is very frustrated with America’s pullout from the TPP. Japan is hoping the TPP could provide them with an advantage over China’s spreading power. After Amerivca’s pullout, the TPP is significantly weaker. Vice President Mike Pence and Agricultural Secretary Sonny Perdue, have tried to soothe the agitation, by hinting at new “beautiful” bilateral trade deals. Mike Pence is hoping Japan will be down for secret under the table deals only between them and America.

However, Japanese officials feel that such negotiations would counter the concept of an international playing field. Any country that flips off the multi-national agreement and instead signs a deal with America, would instantly become ostracized by the world.

the rich asshole became president by appealing to the uneducated farmers and coal miners and promising them to bring them back to prominence. the rich asshole got us out of the Paris Accord Climate, in an attempt toe reinvigorate the coal mining industry. Coal is from last century. In order for us to start using coal again, our entire manufacturing industry would have to be revamped. American factories would have to be willing to pay almost twice as much to use coal as opposed to natural gas. Coal is a thing of the past.

Meanwhile, China is making headlines by becoming the most powerful political force behind the globalization of electric vehicle technology. Experts predict all cars in China will be electric in about ten years. China sells more electric cars than any other nation.

Remember all of those the rich asshole supporters saying how the rich asshole’s business mind is what this country needs? I’m sure all of them right now are nursing plenty of regrets.

According to an explosive new report, President the rich asshole thinks he’ll end up appointing a total of four new Supreme Court Justices by the end of his first term.

When he was asked how he would end up getting to that number, the rich asshole mentioned that he already replaced Antonin Scalia with Neil Gorsuch, and the probability of Justice Anthony Kennedy retiring soon was highly likely.

In his conversation, he made fun of a Justice Ginsburg’s body weight (suggesting it was a reason she would be replaced) and thought President Obama’s latest pick Justice Sonia Sotomayor would be gone soon, too, because of Diabetes.

Per Axios:

“Ok,” one source told the rich asshole, “so that’s two. Who are the others?”

“Ginsburg,” the rich asshole replied. “What does she weigh? 60 pounds?”

“Who’s the fourth?” the source asked.

“Sotomayor,” the rich asshole said, referring to the relatively recently-appointed Obama justice, whose name is rarely, if ever, mentioned in speculation about the next justice to be replaced. “Her health,” the rich asshole explained. “No good. Diabetes.”

For the record, when President Obama appointed Sotomayor, it was already well known she was a life-long diabetic. She has been dealing with the disease since the age of 7 when she first learned of it.

As far as the rich asshole’s comments on Ginsburg, she underwent surgery for colon cancer back in 2009, more than eight years ago, and she’s still around. She’s also currently 84-years-old and works out at a gym inside the Supreme Court.

Her daily workout has even be published online, and a reporter for Politico tried to replicate it. His response? “It nearly broke me.”

We’d like to see the rich asshole try out this workout before talking any more smack.

‘It’s not magic and it’s not true’: MSNBC hosts gleefully blow up the rich asshole’s boast he sent the stock market soaring

MSNBC's Ali Velshi and Stephanie Ruhle -- MSNBC screenshot

DON'T MISS STORIES. FOLLOW RAW STORY!

MSNBC business reporters Ali Velshi and Stephanie Ruhle sarcastically tore apart President some rich asshole’s claims that he has set the stock market on a record path, saying his claims are easily disputed and absolutely “not true.”

On MSNBC’s Velshi & Ruhle, the two hosts took exception with the rich asshole’s claim that the rising stock prices during administration have resulted in lowering the national debt — saying it was nonsense.

“Wrong!” host Ruhle began with a smirk. “The businessman president just flunked a basic finance test. The stock market has nothing to do with the U.S. debt, which continues to go up, not down, despite the president’s best wishes. And I want to remind our viewers that there are only two ways to bring down the national debt: either we cut spending or raise taxes. And guess what we’re doing? Neither of those things!”

“This is a weird one because either the president — he’s a businessman so he can’t not know this is the case — so the assumption becomes that was deliberately false,” co-host Velshi pitched in. “But let’s say he didn’t know. Let’s say he actually thinks that the stock market increasing, which is private money that goes to companies and their shareholders, somehow relates to the debt. Then I don’t know what’s worse, that he was being misleading or what he didn’t know? But either way, this is really serious.”

Taking a harder look at the way the stock market is rising, Velshi noted that the climb began after Democratic President Barack Obama took office and, while the stock market is up, it is also up in other countries.

“Take a look at the rest of the world. The stock markets in most other developed countries are up and, in fact, they are all up in the same time period since some rich asshole has taken office by more than America’s are,” he explained before sarcastically adding, “So, somehow, this magic of some rich asshole is helping the entire developed world’s stock market go up.”

“It’s not magic and it’s not true,” co-host Ruhle added with a laugh.

Watch the video below via MSNBC:

Weinstein takedown leaves the rich asshole sex assault accusers frustrated at lack of justice for themselves

Former Miss Utah Temple Taggart McDowell (Photo: Screen capture)

DON'T MISS STORIES. FOLLOW RAW STORY!

While women in the entertainment industry and beyond may rejoice and feel vindicated by the public downfall of Hollywood producer and sexual predator Harvey Weinstein, BuzzFeed’s Kendall Taggart and Jessica Garrison say that one group of women feels stung by the lack of justice in their own cases.

In 2016, more than a dozen women came forward with stories of sexual harassment, kissing, groping and other inappropriate conduct by then-candidate some rich asshole. the rich asshole denied the allegations and his attorney Marc Kasowitz threatened to sue the women and any publication that ran their stories.

That lawsuit never materialized, but the women who sacrificed their anonymity “watched the man they say humiliated and abused them get elected president of the United States,” said BuzzFeed.

“When he won, I felt like I lost,” said Melissa McGillivray, a Palm Springs, FL photographer’s assistant who said in October of 2016 that the rich asshole “grabbed my a**” at a Mar-a-Lago event.

Now, McGillivray told BuzzFeed, she is living in hiding after getting deluged with hateful abuse and threats of violence for speaking out against the rich asshole. She said the reason Weinstein’s accusers are getting more attention is because they’re wealthy and famous.

“We have women coming out that are celebrities and of course it gets more traction. They have more credibility than I do,” she said.

Temple Taggart McDowell — a former Miss Utah who said last year that the rich asshole repeatedly kissed her on the mouth without her permission — told BuzzFeed that it was gratifying to see Weinstein unseated from his position of power, but it still left her “sad” that when it came to her accusations against the rich asshole, “they brushed it all under the rug.”

Taggart was viciously attacked on social media after she broke her silence.

“It makes you realize why women don’t come forward,” she said.

Jessica Leeds, 70, came forward in 2016 to reveal that the rich asshole groped her during a commercial airline flight.

“A longtime New Yorker, she said that on the streets, she has been greeted with joy and thanks for speaking out. Women have come up to her on the subway and even in the shower at the gym to thank her and extol her bravery. Every woman who came up to her, she said, had their own story of being sexually harassed,” said BuzzFeed.

Leeds, too, was subject to heated abuse after former CNN host Lou Dobbs posted her phone number and contact information online.

She told BuzzFeed that her only regret is that her story “didn’t have more impact.”

“I hoped it did, but it didn’t,” she said.

Weinstein was ousted from the board of the Motion Picture Academy on Saturday.

President the rich asshole defended what he described as America's spiritual bedrock in an impassioned speech to conservative voters in Washington on Friday, pledging to "stop all attacks on our Judeo-Christian values."

the rich asshole was the first sitting president to address the Values Voter Summit, a yearly symposium of socially conservative leaders and voters who aim "to preserve the bedrock values of traditional marriage, religious liberty, sanctity of life, and limited government that make our nation strong."

The ballroom at the Omni Shoreham Hotel in northwest Washington was crowded and raucous during his remarks on Friday, which spanned half an hour and drew repeated standing ovations from the crowd. The speech was characteristic of the rich asshole, who oscillated between the matter at hand — conservative principles — and boasting of his political record since taking office, referring to the growth of U.S. manufacturing and the success of federal disaster management in regions devastated by hurricanes.

But his oration reached a peak when he addressed the challenges he said plague America's Christian conservatives, who made up the majority of Friday's audience.

"We don't worship government, we worship God," the rich asshole said, to loud cheers. "Our founders invoked our creator four times in the Declaration of Independence. And how times have changed. But you know what? Now they're changing back again."

He said that conservative Christian America would enjoy a renaissance with him in the White House.

"We are stopping all our attacks on Judeo-Christian values," the rich asshole said. "We don't use the word Christmas because it’s not politically correct. You’ll go to department stores and they say ‘Happy New Year’ instead.

Under his presidency, the rich asshole promised, "we're saying Merry Christmas again! Our values will endure. Our nation will thrive. Our citizens will flourish, and our freedom will triumph."

the rich asshole also briefly mentioned the unfolding crisis in Puerto Rico, which was severely hit by Hurricane Maria three weeks ago.

"We’re gonna be there. It’s not a question of choice. We love those people," the rich asshole said. "When America is unified, no force can break us apart. We love our families, we love our neighbors, we love our country."

For the audience at the Values Voter Summit, which numbered in the thousands, the rich asshole's speech was the climax of an already raucous assembly of high-profile conservatives. The roster of scheduled speakers includes current and former members of the rich asshole's inner circle — Kellyanne Conway, Steve Bannon, Sebastian Gorka — and right-wing pundits such as Laura Ingraham and Todd Starnes.

the rich asshole: ‘Dems must get smart and deal’ on health-care

BY JULIA MANCHESTER - 10/13/17 09:37 PM EDT

President the rich asshole on Friday ripped Democrats critical of his move to end key payments to insurers selling ObamaCare plans, saying lawmakers from the opposing party must "get smart & deal."

"Money pouring into Insurance Companies profits, under the guise of ObamaCare, is over. They have made a fortune. Dems must get smart & deal!" the rich asshole wrote on Twitter.

"ObamaCare is causing such grief and tragedy for so many. It is being dismantled but in the meantime, premiums & deductibles are way up!" he added in another tweet.

Money pouring into Insurance Companies profits, under the guise of ObamaCare, is over. They have made a fortune.

Dems must get smart & deal!

Dems must get smart & deal!

ObamaCare is causing such grief and tragedy for so many. It is being dismantled but in the meantime, premiums & deductibles are way up!

the rich asshole's comments came a day after the White House said the administration would end the disbursements to insurance companies, known as cost-sharing reduction (CSR) payments.

The payments are aimed at helping low-income people afford co-pays, deductibles and other out-of-pocket costs associated with health-insurance policies.

the rich asshole has repeatedly threatened to cut off the payments, which have been made on a monthly basis. Critics condemned his move late Thursday to eliminate the funding, his most aggressive move yet to dismantle ObamaCare.

Some Republicans criticized the move, with Nevada Gov. Brian Sandoval (R) calling the rich asshole's decision "devastating" and Rep. Ileana Ros-Lehtinen (R-Fla.) saying the move does not lead to increased access to health insurance.

Eighteen states and Washington, D.C., filed lawsuit in federal court in California on Friday to block the rich asshole from halting the payments, while Democratic leaders called for Congress to quickly move to restore the payments, potentially through must-pass legislation later this year.

the rich asshole has made a push on health-care after GOP efforts to repeal ObamaCare failed this year. The president phoned Senate Minority Leader Charles Schumer (D-N.Y.) last Friday, saying he hoped to start a dialogue on health-care. Schumer later said that the rich asshole wanted to make another push for ObamaCare repeal, which the Democratic leader said was "off the table."

the rich asshole acts alone to destroy Obamacare

WASHINGTON -- President the rich asshole has made a lot of promises on health care.

Somehow, though, I don't remember him promising stadiums of cheering fans that he'd take away protections for pre-existing conditions, increase deductibles, spike premiums, eliminate basic coverage requirements and, more generally, destabilize the individual health-insurance market.

But that is what he said he'd do Thursday, when he signed an executive order on health care.

Those aren't the precise words he used, of course. But they are the consequences of the policy bombs he wants to set off in two relatively obscure corners of the insurance market: association health plans and short-term health plans.

Under current law, an association of small businesses (such as a group of law firms) can band together and market insurance to members. These association health plans must abide by all the consumer protections of the Affordable Care Act. They are also subject to the insurance laws and rules of the state in which they're sold.

But under the rich asshole's executive order, depending on what the final regulations say, an association could exempt itself from lots of federal Obamacare requirements (such as essential health benefits) and choose any state to be its regulator (regardless of where its members are).

Meaning if it wanted to be regulated by a state that doesn't require coverage of prescription drugs or cancer treatments, it could.

This would not only rob states of their sovereignty, which Republicans have so often claimed to champion, but also create a race to the bottom. Pursuing ever-lower premiums, every association would likely incorporate in the most Wild-West-like state around, in the way that credit card companies tend to domicile in South Dakota.

The administration has also left open the possibility that individuals -- and not just small employers -- could buy into these association plans, further siphoning people out of the individual markets.

"Short-term health plans" can sometimes serve a legitimate purpose -- a stopgap to tide you over for the summer until the school year starts, for instance. But after Obamacare passed, there was a proliferation of scammy "short-term" plans that weren't so short term. Some lasted 364 days! Why? Because technically, they weren't considered insurance and weren't subject to Obamacare consumer protections. Insurers could offer skimpy plans and cherry-pick the cheapest, most profitable enrollees.

The Obama administration ultimately closed this loophole by determining that short-term plans must be shorter than three months. With his executive order, the rich asshole seeks to re-lengthen those plans.

Two main problems result.

One is that, absent minimums for quality and regulatory oversight, lots of Americans are likely to get conned into plans that cover almost nothing. These are sometimes called min-med or "buffalo plans," because they pay out pretty much only if you're trampled by a herd of buffalo.

The bigger problem is called adverse selection. Healthy people will sort into low-cost, bare-bones plans, while relatively costly people will stay in the more generous, Obamacare-compliant plans, which can't legally turn customers away. Premiums in Obamacare plans would then spike, driving out more relatively healthy people, further driving up premiums, and so on.

In the end, the whole individual market falls apart, leaving us with basically the pre-Obamacare system. Even those healthy people -- even if they stay healthy! -- have no real options.

The only good news is that the rich asshole's executive order doesn't have force of law. It's a set of instructions for Cabinet members to come up with further regulations. In the meantime, though, they'll spook a lot of insurers, which have only just recently found their footing in the existing system. And it's also likely to confuse consumers, which will depress enrollment and destabilize markets further.

And late Thursday night, he announced that he won't pay crucial subsidies to help lower-income people pay for out-of-pocket care, knocking yet another pillar out from under Obamacare.

Which would be pretty much on brand for this nihilistic president: When you can't come up with a new system that works, just blow up the old one.

Catherine Rampell is a columnist for the Chicago Tribune.

the rich asshole scraps Obamacare subsidies in surprise late-night announcement

Federal payments underpinning healthcare scheme unlawful, says White House, in move that takes a further swipe at Democrats’ signature reform

some rich asshole has planted a timebomb under Obamacare, issuing a notice late on Thursday night that scraps vital federal subsidies underpinning the current healthcare system.

The late-night move caught critics off guard and brought immediate accusations that the rich asshole was unilaterally destroying his predecessor’s signature legislation, the Affordable Care Act, after the Republican-controlled Congress failed to secure changes. The announcement stops federal support of up to $7bn (£5.27bn) to insurance companies to help them cover the medical needs of low-income Americans.

The rich asshole administration sought to lay the blame for the current crisis in healthcare on former president Barack Obama, claiming the federal subsidies, known as “cost-sharing reduction payments”, were unlawful and “yet another example of how the previous administration abused taxpayer dollars and skirted the law to prop up a broken system”.

On Friday morning the rich asshole claimed in a tweet that “the Democrats [sic] ObamaCare is imploding” and appeared to call on the Democrats to negotiate with him over healthcare legislation.

“Massive subsidy payments to their pet insurance companies has stopped,” he wrote. “Dems should call me to fix! ... ObamaCare is a broken mess. Piece by piece we will now begin the process of giving America the great HealthCare it deserves!”

Reaction from Democratic politicians and other the rich asshole opponents was swift. Top officials on both coasts leapt to denounce the White House move and threaten legal action to stop the subsidies being revoked.

In California, the state attorney general Xavier Becerra said he was prepared to sue the the rich asshole administration to protect the subsidies. Eric Schneiderman, the attorney general of New York state, followed suit, declaring he would “not allow President the rich asshole to once again use New York families as political pawns in his dangerous, partisan campaign to eviscerate the Affordable Care Act at any cost”.

The attack on the federal subsidies came as a double blow to Obamacare, just hours after the rich asshole had already lashed out at his predecessor’s healthcare reforms by issuing an executive order unilaterally weakening the system. In that order, the president opened the door to cheaper and less comprehensive insurance, which experts predict will result in health plans for the sick becoming more expensive.

Thursday night’s second blow could prove the more deadly of the two as it is targeted at the very foundations of the insurance structures created under Obamacare. A study by the Congressional Budget Office two months ago suggested that terminating the cost-sharing subsidies would lead to a dramatic 20% rise in the average cost of the most popular plans offered by the Affordable Care Act, as well as worsening the federal deficit by almost $200m.

Even moderate conservative voices were aghast by the move. Charlie Sykes, a prominent conservative talkshow host, said: “What we have now, for better or worse, is Trumpcare. the rich asshole has said he wants Obamacare to implode. Is now taking steps to make it implode. Now owns all of the consequences.”

Among Republican leaders in Congress, the speaker of the House of Representatives came to the rich asshole’s support, even though his own party had failed to find a workable replacement for Obamacare. Paul Ryan said the president’s efforts to unpick Obama’s reforms marked a “monumental affirmation of Congress’s authority … Obamacare has proven itself to be a fatally flawed law”.

the rich asshole had earlier hailed his changes as a step that “will cost the United States government virtually nothing and people will have great, great healthcare. And when I say people, I mean by the millions and millions.”

The administration has taken other steps to derail the ACA: cutting the sign-up period for insurance by half; shutting down for maintenance the website people use to sign up for health insurance; slashing funding for outreach; and repeatedly threatening to end subsidies to insurance companies that cover the poor.

the rich asshole acknowledged efforts to repeal and replace the ACA through legislation had been thwarted not just by Democrats but “a very small, frankly, handful of Republicans”. He said: “We will fix that.”

‘Complete moron’: Internet ridicules the rich asshole for saying he spoke to ‘the President of Virgin Islands’ — aka himself

some rich asshole looks at a mask of himself (CSPAN / YouTube)

DON'T MISS STORIES. FOLLOW RAW STORY!

some rich asshole on Friday spoke at the social conservative Values Voters summit, extolling the virtues of his presidency, as well as his administration’s response to a number of catastrophic natural disasters that have ravaged the nation.

“I will tell you, I left Texas, and I left Florida, and I left Louisiana, and I went to Puerto Rico, and I met with the president of the Virgin Islands,” the rich asshole exclaimed during his speech.

Seemingly unbeknownst to him, the president of the Virgin Islands—a U.S. territory—is, in fact, some rich asshole.

The White House quickly tried to clean up the president’s remark, releasing a transcript of his speech with “president” scratched out and “governor” written beside it in parenthesis.

But it was not fast enough for the Internet, which went on to ridicule the rich asshole for not knowing he’s the president of the Virgin Islands, too.

Read some responses below, via Twitter:

I really hope @realDonaldTrump told the president of the Virgin Islands how much of a dick he is.

Hard to believe that you didn't know that you're the President of the U.S. Virgin Islands. twitter.com/realdonaldtrum…

Exclusive photo of Trump meeting with the "president of the Virgin Islands" twitter.com/hashtagcutebut…

Then he's talking to himself. Because he's the president of the Virgin Islands. twitter.com/zekejmiller/st…

Were you looking in the mirror @realDonaldTrump? YOU are the president of the AMERICAN Virgin Islands. How much more of this can we take?!!! twitter.com/zekejmiller/st…

")

He doesn't know that he's the president of the US Virgin Islands. He doesn't know it's not a separate country. twitter.com/ZekeJMiller/st…

He meets the president of the Virgin Islands daily, in fact twitter.com/ZekeJMiller/st…

. @realDonaldTrump, our existential president, met with President of Virgin Islands. 'Great guy, tremendous, media so unfair to him too'

Trump says he met with the president of the Virgin Islands, which is him. He’s a complete moron. #25thAmendmenttwitter.com/i/moments/9188…

The Virgin Islands are on an alternate timeline where things are much better. twitter.com/davidmackau/st…

")

Pentagon forwarded reporter its plan to spin Puerto Rico as ‘a success’ and ignore San Juan’s mayor

President some rich asshole speaks during a briefing on Hurricane Maria relief efforts (Screenshot)

DON'T MISS STORIES. FOLLOW RAW STORY!

Late in September, Bloomberg News climate reporter Christopher Flavelle inadvertently received a series of emails meant for Pentagon employees — emails that detailed the federal plan to spin President some rich asshole’s bungling of the response to Hurricane Maria and to dismiss criticisms from San Juan’s firebrand Mayor Carmen Yulín Cruz.

According to Flavelle, when he notified Defense Department officials, he still continued to receive the bulletins for five days.

“Those messages, each of which was marked ‘unclassified,’ offer a glimpse into the federal government’s struggle to convince the public that the response effort was going well,” Flavelle said Friday. “That struggle was compounded by the commander-in-chief, and eased only when public attention was pulled to a very different disaster.”

He went on to list dates, the news events that took place and the Pentagon’s response plan.

“Sept. 28: Eight days after Maria hit, coverage of the federal government’s response is getting more negative,” Flavelle said. “The Government Message: Pentagon officials tell staff to emphasize ‘coverage of life-saving/life-sustaining operations’ and for spokespeople to avoid language about awaiting instructions from FEMA, ‘as that goes against the teamwork top-line message.’”

On Sep. 30, the rich asshole attacked Mayor Yulín Cruz as a “poor leader” and Pentagon officials fretted that the president’s “lack of empathy” was becoming the front-page story, so the response was to hammer on the message that FEMA has been successful at reaching “all municipalities in Puerto Rico.”

Notably, FEMA has still not provided relief supplies to the furthest western reaches of the island, where people are dying of water-borne diseases and struggling to survive.

On Oct. 1, the rich asshole called his critics “politically-motivated ingrates”. On that day, the Pentagon’s message was, “Defense staff admit that ‘the perception of USG response continues to be negative.’ Spokespeople are told to say, ‘I am very proud of our DOD forces,” before conceding “there are some challenges to work through.’”

All American Citizens will be Required to say “Merry Christmas” as the rich asshole calls for Total Support of Evangelicals

Friday, 13 October 2017

the rich asshole will no longer allow attacks and criticism of Evangelicals in what he said that will be an attack on “our American heritage and traditions.”

“We are stopping cold the attacks on Judeo-Christian values.” the rich asshole said to pomp and applause before laying hard into the people who don’t say “Merry Christmas”.

Speaking to a Conservative Conference known as the Values Voter Summit, the rich asshole promise to return America to its glory and put an end to all political correctness.

“They don’t use the word Christmas because it is not politically correct,” the rich asshole said, complaining that department stores will use red and Christmas decorations but say “Happy Holidays.” “We are saying Merry Christmas again!”

The fiery speech drew much applause and support among Evangelicals across America who are the core base of the rich asshole’s support.

This latest announcement seems like a fulfillment of one of his campaign promises. As Presidential candidate in 2016, the rich asshole promised to bring back Merry Christmas and stop political correctness.

“You go into a department store. When was the last time you saw ‘Merry Christmas’? You don’t see it anymore,” the rich asshole said on the campaign trail. “They want to be politically correct. If I’m President, you will see ‘Merry Christmas’ in department stores, believe me, believe me.”

“America is a nation of believers and we are strengthened and sustained by the power of prayer,” the rich asshole said.

While he spoke about bringing back Merry Christmas, many were unaware that the rich asshole had just ended insurance subsidies for the poor and low income earners.

the rich asshole has rolled back an Obamacare principle that required employers to provide birth control coverage as part of their health insurance policies.

While the rich asshole attacks birth control coverage which is a vital part of women’s health, he refuses to scrap the policies that even in the Public sector are spending millions of dollars on viagra and other sex enhancement drugs.

The State Department and the Pentagon are reported to be spending millions of dollars a year on viagra alone.

the rich asshole Administration Tries To Fix His Dumbest Statement Yet, Fails MISERABLY (IMAGE)

some rich asshole’s administration is probably the most stressed out team the White House has ever seen. While dealing with multiple ethical issues and investigations, the administration never gets a day of rest as they are in constant reaction mode and doing damage control on his constant blunders. Today was the perfect example of an administration that is hanging on by a thread.

Earlier today, the rich asshole displayed his blatant stupidity as he gave a speech at the conservative Values Voter Summit. During that speech, the rich asshole shocked over 3,000 attendees (and the world) when he said he’d met with the “president of the Virgin Islands.” This was the rich asshole’s direct quote:

“I went to Puerto Rico, and I met with the president of the Virgin Islands, these are people that are incredible people. They’ve suffered gravely, and we’ll be there. We’re gonna be there. We have, really, it’s not even a question of a choice … we’re going to be there as Americans.”

the rich asshole apparently doesn’t know that HE is the president of the Virgin Islands, because the islands are a part of American territory! As expected, Twitter dragged the rich asshole for this:

There’s really no way to gracefully fix this, but still the rich asshole administration had to try. In a half-ass, hilarious attempt to minimize the rich asshole’s very obvious f*ck up, the White House released a transcript of the rich asshole’s remarks – and crossed out the word “president” and replaced it with the correction of “governor of the Virgin Islands.” CNN’s Kaitlan Collins made sure to share this with everyone:

It’s like the rich asshole administration didn’t even try to be subtle! And how could they? Just as they put out one fire, the rich asshole is making five more. the rich asshole’s team doesn’t have time or the energy to keep cleaning up his messes – and this pathetic attempt is direct proof!

the rich asshole on pace to double Obama’s executive order tally

Jason Le Miere

Posted with permission from Newsweek

From the comfort of his reality TV-host perch, Donald Trump slammed then-President Barack Obama over his use of executive orders. Once in the White House, though, Trump has done the exact thing for which he criticized his predecessor—on a range of issues, from golfing days to attacking Syria to, yes, signing executive orders. Indeed, not only has he failed to reverse course, he has gone much further than Obama.

elated: Donald Trump signed an executive order on Obamacare, but is it legal?

On Thursday, Trump signed an executive order undoing part of the Obamacare law, which he claimed would expand the availability of affordable health care. Democrats asserted it amounted to sabotaging Americans with pre-existing conditions.

The executive order was significant in another way, too: It was the 50th Trump has signed as president. By comparison, Obama had signed just 26 at this point of his presidency. He would eventually average 35 a year during his eight years in the White House—the fewest of any president for 120 years—en route to a total of 277. Trump is currently on pace to sign 275 executive orders. In one term.

Obama's relatively low figure did not prevent Trump from repeatedly deriding him for what he called “major power grabs of authority.” Illustrating that this is a longstanding complaint of Trump's, that tweeted comment was made in July 2012.

It was a message that Trump expanded upon with vigor when on the campaign trail.

“I don't think he even tries anymore. I think he just signs executive actions,” Trump said at a campaign event in December 2015 before criticizing what he deemed Obama’s failure to adhere to the proper checks and balances. “That's the way the system is supposed to work. And then all of a sudden, I hear he tried, he can't do it, and then, boom, and then another one, boom.”

The theme was one Trump returned to many times before he entered the White House.

“Obama goes around signing executive orders,” Trump said in February 2016. “He can't even get along with the Democrats. He goes around signing all these executive orders. It's a basic disaster. You can't do it.”

The words have come back to haunt the Republican president. A failure to get his own party to act in line with his wishes has directly led to many of his executive orders, including the most recent. Thursday’s signing followed the failure of Republicans to repeal and replace Obamacare, something that provoked the president into a very public outpouring of frustration.

With the public sniping between the president and members of his own party only increasing, there is every chance that, should he want to advance his agenda, Trump's accelerated executive-order-signing pace will only continue.

elated: Donald Trump signed an executive order on Obamacare, but is it legal?

On Thursday, Trump signed an executive order undoing part of the Obamacare law, which he claimed would expand the availability of affordable health care. Democrats asserted it amounted to sabotaging Americans with pre-existing conditions.

The executive order was significant in another way, too: It was the 50th Trump has signed as president. By comparison, Obama had signed just 26 at this point of his presidency. He would eventually average 35 a year during his eight years in the White House—the fewest of any president for 120 years—en route to a total of 277. Trump is currently on pace to sign 275 executive orders. In one term.

Obama's relatively low figure did not prevent Trump from repeatedly deriding him for what he called “major power grabs of authority.” Illustrating that this is a longstanding complaint of Trump's, that tweeted comment was made in July 2012.

It was a message that Trump expanded upon with vigor when on the campaign trail.

“I don't think he even tries anymore. I think he just signs executive actions,” Trump said at a campaign event in December 2015 before criticizing what he deemed Obama’s failure to adhere to the proper checks and balances. “That's the way the system is supposed to work. And then all of a sudden, I hear he tried, he can't do it, and then, boom, and then another one, boom.”

The theme was one Trump returned to many times before he entered the White House.

“Obama goes around signing executive orders,” Trump said in February 2016. “He can't even get along with the Democrats. He goes around signing all these executive orders. It's a basic disaster. You can't do it.”

The words have come back to haunt the Republican president. A failure to get his own party to act in line with his wishes has directly led to many of his executive orders, including the most recent. Thursday’s signing followed the failure of Republicans to repeal and replace Obamacare, something that provoked the president into a very public outpouring of frustration.

With the public sniping between the president and members of his own party only increasing, there is every chance that, should he want to advance his agenda, Trump's accelerated executive-order-signing pace will only continue.

World governments fear the rich asshole will convince Iran to restart nuclear program

President some rich asshole refused to certify the 2015 Iran nuclear agreement. (AFP / Brendan SMIALOWSKI)

DON'T MISS STORIES. FOLLOW RAW STORY!

President some rich asshole launched a tougher strategy to check Iran’s “fanatical regime” on Friday and warned that a landmark international nuclear deal could be terminated at any time.

In a much-anticipated White House speech, the rich asshole stopped short of withdrawing from the 2015 accord, but “decertified” his support for the agreement and left its fate in the hands of Congress.

And, outlining the results of a review of efforts to counter Tehran’s “aggression” in a series of Middle East conflicts, the rich asshole ordered tougher sanctions on Iran’s Revolutionary Guards Corps and on its ballistic missile program.

the rich asshole said the agreement, which defenders say was only ever meant to curtail Iran’s nuclear program in return for sanctions relief, had failed to address Iranian subversion in its region and its illegal missile program.

The US president said he supports efforts in Congress to work on new measures to address these threats without immediately torpedoing the broader deal.

“However, in the event we are not able to reach a solution working with Congress and our allies, then the agreement will be terminated,” the rich asshole said, in a televised address from the Diplomatic Room of the White House.

“It is under continuous review and our participation can be canceled by me as president at any time,” he warned.

Simultaneously, the US Treasury said it had taken action against the Islamic Revolutionary Guards under a 2001 executive order to hit sources of terror funding and added four companies that allegedly support the group to its sanctions list.

the rich asshole’s criticism of the so-called Joint Comprehensive Plan of Action (JCPOA) — the nuclear control accord reached between Iran and Britain, China, France, Germany, Russia and the United States — had raised global concerns.

World governments feared any US move to sabotage the arrangement could dash Washington’s diplomatic credibility and relaunch Iran’s alleged quest for a nuclear weapon, in turn provoking a new Middle East arms race.

But Secretary of State Rex Tillerson made clear ahead of the president’s speech that his decision does not necessarily mean an end to the accord.

– ‘The worst deal’ –

“The intent is that we will stay in the JCPOA, but the president is going to decertify,” Tillerson said.

“We’re saying, fine, they’re meeting the technical compliance,” he said, indicating that the broader agreement would remain intact for now, and that US lawmakers will have an opportunity to revisit the US sanctions regime.

the rich asshole had repeatedly pledged to overturn one of his predecessor Barack Obama’s crowning foreign policy achievements, deriding it as “the worst deal” and one agreed to out of “weakness.”

The agreement stalled Iran’s nuclear program and marginally thawed relations between Iran and what Tehran dubs the “Great Satan,” but opponents, and even some supporters, say it also prevented efforts to challenge Iranian influence across the Middle East.

But since coming to office, the rich asshole has faced intense lobbying from international allies and much of his own national security team, who argue the JCPOA should remain in place.

Both the US government and UN nuclear inspectors say Iran is meeting the technical requirements of its side of the bargain, dramatically curtailing its nuclear program in exchange for sanctions relief.

US concerns about the Guards could also weaken the deal. the rich asshole stopped short of designating the powerful military faction a global terror organization, as some hawks demanded, but his announcement of targeted sanctions is still likely to trigger an angry Iranian response.

Apart from running swaths of Iran’s economy and Iran’s ballistic program, the corps is also accused of guiding bellicose proxies from Hezbollah in Lebanon, to the Huthi in Yemen to Shiite militia in Iraq and Syria.

“We have considered that there are particular risks and complexities to designating an entire army, so to speak, of a country,” Tillerson said.

Instead the US will squeeze those directly supporting the corps’ “terrorist activities, whether it’s weapons exports or it’s weapons components, or cyber activity, or it’s movement of weapons and fighters around.”

– Snap back –

Still, the rich asshole’s tough-guy approach could yet risk undoing years of careful diplomacy and increasing Middle East tensions.

Iranian President Hassan Rouhani lashed out at his US counterpart saying he was opposing “the whole world” by trying to abandon the landmark nuclear agreement.

“It will be absolutely clear which is the lawless government. It will be clear which country is respected by the nations of the world and global public opinion,” he added.

Congress must now decide whether to end the nuclear accord by “snapping back” sanctions, which Iran demanded be lifted in exchange for limiting uranium enrichment.

the rich asshole will not ask Congress to do that, Tillerson said. “A re-imposition of the sanctions,” he said, “would, in effect, say we’re walking away from the deal.”

But lawmakers may yet decide to torpedo the agreement.

Proposals by Republican Senators Tom Cotton and Bob Corker to introduce “trigger points” for new sanctions and extend sanctions beyond a pre-agreed deadline have spooked allies, who believe it could breach the accord.

But it remains unclear if their proposals can garner the 60 votes need to pass the Senate.

Our embarrassing president thinks the natural rights of Americans are like a buffet

President some rich asshole speaks shortly after arriving in Ft. Meyers, Fla., Sept. 14, 2017. The event was the first stop on a visit to thank first responders and meet with victims of Hurricane Irma. (Coast Guard photo by Petty Officer 1st Class Patrick Kelley.)

DON'T MISS STORIES. FOLLOW RAW STORY!

some rich asshole unloaded a tweetstorm this morning about Puerto Rico’s continuing recovery after Hurricane Maria that managed to appall even after all these months of being appalled by what this president is willing to say.

I’m not going to talk about how racist it is. Many writers of color—who are smarter than I am and more authoritative than I am on matters of white supremacy—are going to talk about it. I’ll defer to them, and a lot of other white people should too.

What I want to talk about is the obligation of the office of the presidency—to defend and protect not only the U.S. Constitution, but every single American’s right to life, liberty, and the pursuit of happiness. (Puerto Ricans are indeed U.S. citizens.)

More precisely, I want to talk about why the office of the president is supposed to do those things. To that end, let’s remember the works of John Locke, the English philosopher who left an indelible mark on the Founders’ thinking, especially Thomas Jefferson’s.

Locke believed all of us are born free and equal, and that governments must be constituted to protect those natural rights. The Founders added Hobbes and Montesquieu to conclude that government’s goal is also to protect the weak from the strong. Part of its mandate is to defend against a state of nature.

I presume neither the Enlightenment philosophers nor the Founders were thinking about cataclysmic hurricanes when they pondered the need for government to protect against a state of nature, but that’s surely the kind of thinking we need now that much of Puerto Rico remains without power and without adequate supplies of food and water. Hurricane Maria destroyed the island’s infrastructure as well as its agriculture—Puerto Rico is going to need huge investments.

Yet this morning, the president said in so many words that Puerto Rico was a disaster before the hurricanes hit, and that the federal government can’t stay to provide aid forever. Puerto Rico, the rich asshole implied, will have to take care of itself.

Like I said, I’m not going to talk about the white supremacy of his tweetstorm. My point is the president is saying the natural rights of people born free and equal are like a buffet. The government can pick and choose whose rights to protect, and throw away the rest.

And my point is he’s saying this out loud, an important nuance. the rich asshole is not the first or last president to chafe at the idea of serving Americans who despise him personally and politically. This is not to say presidents should not give special attention to their supporters and allies. But no president in my lifetime has actually said this in public. That matters, because what the rich asshole says in public influences what he’s willing to accept in terms of policy outcomes.

Puerto Rico isn’t alone. The AP reported Wednesday some 3,500 homes and buildings have been consumed by wildfire in the Napa Valley. The conflagration comes after long summer months, during which fires raged in California. Yet the president has said nothing.

This is a big deal and it can’t be overstated. Most people are going to focus on the president’s moral obligation to help. But considering the damage in Puerto Rico and California, the need for recovery goes beyond morals. the rich asshole is not the president of only red states. He has a constitutional obligation to “preserve, protect and defend.”

WATCH: the rich asshole ‘invents another African country’ by butchering pronunciation of Tanzania

some rich asshole (Image via Gage Skidmore) and the Tasmanian Devil (Image via Twitter)

DON'T MISS STORIES. FOLLOW RAW STORY!

In his second public speech of the day, some rich asshole on Friday continued not-quite-reading off teleprompters, this time mispronouncing the African country “Tanzania” so it rhymed with the Australian island state Tasmania.

The president pronounced “Tanzania” as “Tan-ZAY-nee-uh,” as opposed to the country’s actual pronunciation, “Tan-zu-KNEE-uh.” The flub came just hours after the rich asshole said he spoke with “the President of the Virgin Islands,” who is himself.

It’s not the first time the rich asshole’s mispronounced the word; as candidate, he likewise lacked a grasp of the phonetics of the word, of which assistant professor of African history at Boston College Priya Lal said there’s “no debate.”

“I would say that it really doesn’t bode well if somebody who’s campaigning to be the leader of the United States can’t even pronounce the name of the country,” she told the Guardian. “That seems like the most basic starting point, it is a serious error and it is ignorant.

Internet users were quick to mock the president for his pronunciation:

@realDonaldTrump Ummmm that's not how you pronounce Tanzania. But it doesn't matter. Your zealot supporters tell me you're "smart".

Canada and Mexico stick to their guns on NAFTA despite the rich asshole threats

Canada's Prime Minister Justin Trudeau (L) and Mexican President Enrique Pena Nieto pose for a photo at the presidential palace in Mexico City, on October 12, 2017. (AFP / Alfredo ESTRELLA)

DON'T MISS STORIES. FOLLOW RAW STORY!

The leaders of Canada and Mexico stuck to their upbeat view on the future of the North American Free Trade Agreement on Thursday, despite US President some rich asshole’s threats to axe it.

Visiting Mexico on the heels of a tense trip to Washington, Canadian Prime Minister Justin Trudeau downplayed the rich asshole’s attacks on NAFTA as part and parcel of the negotiations on updating the 23-year-old accord.

“We will not be walking away from the table based on proposals put forward,” he said when asked about the rich asshole administration’s push to include a “sunset clause” requiring the three member countries to unanimously renew the deal every five years.

“We will discuss those proposals, we will counter those proposals and we will take seriously these negotiations,” he told a press conference at the presidential palace after being welcomed with military honors.

Speaking alongside him, Mexican President Enrique Pena Nieto insisted the deal remained vital to the region’s economies, despite the rich asshole’s repeated NAFTA bashing.

But he said Mexico would not be pushed around.

“Mexico is betting on achieving a good agreement. But it will have to be a positive agreement, and good for all three sides, not just one. We won’t be hostage to a single point of view,” he said.

The comments came as negotiators from the three countries meet in the United States for their latest round of what the rich asshole vowed would be tough talks on a new version of NAFTA.

the rich asshole has put both Mexico and Canada on the defensive over trade, accusing the former of taking American jobs and the latter of unfair subsidies, and wants to either overhaul or “terminate” NAFTA.

His administration has land-mined the renegotiation he triggered with controversial proposals, including tightening the “rules of origin” to demand certain amounts of American-made content in products, scrapping NAFTA’s dispute resolution mechanism and the “sunset clause.”

Trade was a touchy subject during Trudeau’s visit to Washington, after the US slapped a 220 percent retaliatory duty on Canadian planemaker Bombardier’s CS100 and CS300 aircraft over dumping allegations.

Trudeau in turn threatened to cancel a purchase of 18 fighter jets from American aerospace giant Boeing, saying he had told the rich asshole he “disagreed vehemently” with the US decision.

– Canadian-Mexican bromance? –

Making his first official visit to Mexico, the prime minister appeared to be looking for a friendly ear in Pena Nieto, himself no stranger to hostility from the the rich asshole administration.

Despite their common ground, however, Canada and Mexico are also at odds on some key issues.

Canada, which shares Washington’s concern over competition from cheap Mexican labor, is notably pushing for Mexico to improve workers’ wages under the new NAFTA — something the Pena Nieto administration says should be determined by the market, not dictated by a trade deal.

Pena Nieto sought to send a message that Mexico and Canada are better off working together as they forge ahead in the delicate negotiations with the giant and sometimes grumpy neighbor they both share.

“Canada and Mexico are going through one of the best moments of our relationship,” he wrote in an op-ed published in Canadian newspaper The Globe and Mail.

“The government of Mexico will keep working constructively with Canada to further strengthen our relations, achieve mutual benefits and contribute to reaching our shared goal: to make North America the most prosperous and competitive region in the world.”

On Friday, Trudeau will wrap up his North American tour with a speech to the Mexican senate, whose approval is needed to ratify any renegotiated version of NAFTA.

Mexico and Canada do some $20 billion a year in bilateral trade.

The figure is dwarfed by their trade with the US: more than $480 billion last year for Mexico and more than $540 billion for Canada.

‘They treat us as others’: Puerto Rican lawmaker hammers GOP for ‘racist’ double standard on storm victims

New York City Speaker Melissa Mark-Viverito -- screenshot

DON'T MISS STORIES. FOLLOW RAW STORY!

Appearing on CNN, Friday morning, New York City Speaker Melissa Mark-Viverito accused President some rich asshole of being a racist who treats Puerto Ricans as “others” and not as Americans.

Speaking with host Chris Cuomo on New Day, Mark-Viverito addressed the rich asshole’s comments that FEMA workers can’t help Puerto Rican survivors of Hurricane Maria “forever” by noting that many victims of the hurricane have yet to see any help.

“Did you come back from Puerto Rico saying, ‘Boy, that’s a success story?'” host Cuomo asked.

“Definitely not,” the lawmaker replied. “It is outrageous and what I call benign neglect. It is level of disinterest to deal with this in a focused way. We don’t have the level of resources when I look at it at face value in the research and looking at the details. But what Florida received after Irma, what Texas received after Harvey, the level of focus and attention, FEMA resources.”

Prodded by the CNN host, Mark-Viverito got around to the root cause of the rich asshole’s seeming indifference to the island of Puerto Rico.

“I’ve been saying that the messages from this present have been sadistic,” the lawmaker explained. “When it comes to the people of Puerto Rico, we have to be very clear — we are being treated like second-class citizens despite the fact that we have had U.S. citizenship for over 100 years.”

“I heard some of the interviews with Republican congressmen, and they see us as others, as somehow foreigners. That they don’t have a responsibility to these U.S. citizens, some of whom have given their lives for this country.” she continued. “There is a real double standard which I think has racist undertones.”

Watch the video below via CNN:

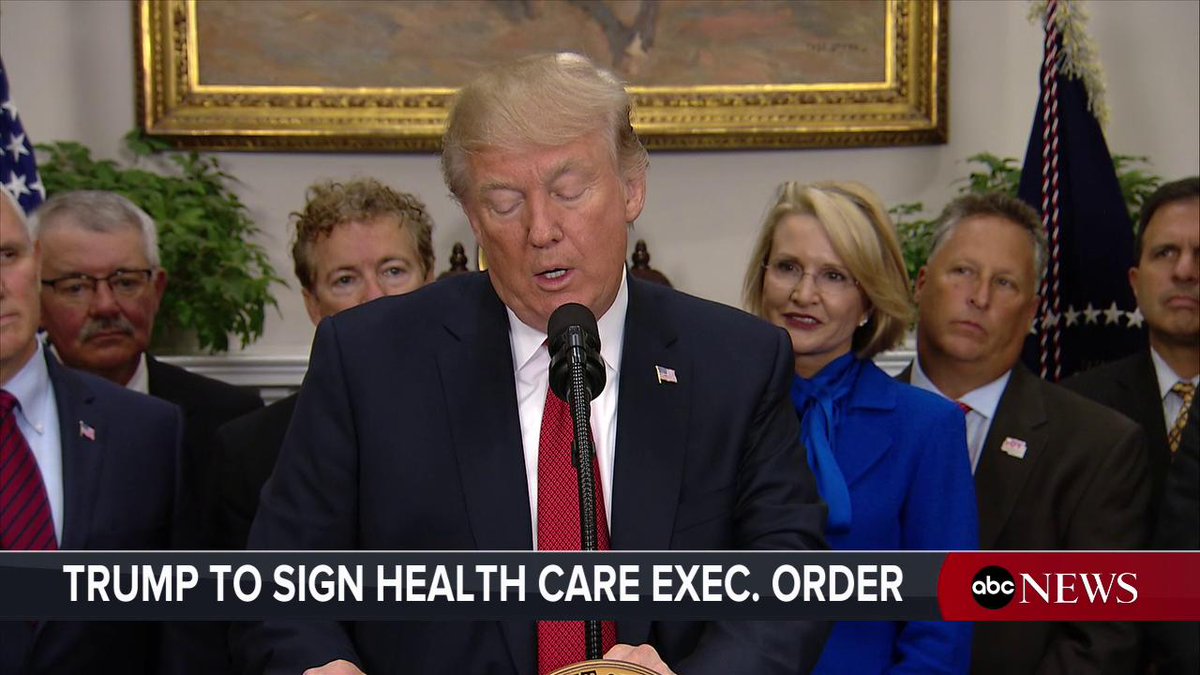

Here’s how the rich asshole’s executive order may compound the health insurance industry’s problems

U.S. President some rich asshole speaks before signing an executive order, making it easier for Americans to buy bare-bone health insurance plans and circumvent Obamacare rules at the White House in Washington, U.S., October 12, 2017. (REUTERS/Kevin Lamarque)

DON'T MISS STORIES. FOLLOW RAW STORY!

AP Photo/Evan Vucci

President some rich asshole has issued the first of what promises to be a series of health insurance executive orders aimed at dismantling the Affordable Care Act.

It instructs the government to essentially exempt small businesses and potentially individuals from some of the rules underpinning the landmark legislation known as “Obamacare,” following the GOP’s failure to get Congress to approve a plan to repeal and replace it.

These steps would free more employers to access bare-bones and short-term health insurance coverage and join together to bargain with insurers. It’s not clear how this order will change the U.S. health insurance market. But as a health finance professor and the former CEO of an insurance company, I’m confident it is more likely to compound many of Obamacare’s problems than to fix them.

AP Photo/Alan Diaz

Designed this way

To be sure, the Affordable Care Act has problems. For example, premiums have continued to rise since the Affordable Care Act’s enactment – albeit at a moderate pace for insurance obtained through employment.

In particular, many smaller employers have seen their costs rise dramatically since insurers were forced to price their plans based on the average of all claims in the small group market rather than the experience of each firm.

But there is a reason why Obamacare was designed this way. Employers with older and less healthy workers were almost shut out of the insurance market because insurers deemed them so costly to cover and wanted to avoid the risk. Companies with younger and healthier workers had a good deal previously, but many other employers did not.

The Affordable Care Act was supposed to solve this problem by lumping everyone together to even out rates. Making rates more reasonable for many Americans meant requiring some of us to pay more.

Market dynamics

The government’s attempt to keep President Barack Obama’s oft-repeated promise that “if you like your current plan, you can keep it” didn’t help. Employers with low-cost plans and healthier workforces chose to be grandfathered out of many new requirements, leaving a much less healthy – and more expensive to cover – pool for pricing everyone else’s insurance.

Nevertheless, the share of adults without health insurance fell to a record low of 10.9 percent in late 2016, from 18 percent before the health insurance exchanges opened in October 2013, as measured by polling by Gallup and Sharecare. (The uninsurance rate has ticked up to 11.7 percent since the rich asshole took office.)

What would be a good way to get the remaining 28 million Americans insured at a reasonable cost? It may seem obvious that letting small businesses without much purchasing power in the health insurance market band together will enable them to get the same deals as large self-insured companies – which get to choose among a variety of options.

In most markets, this kind of diversity and choice fosters the robust competition the rich asshole says he wants to see. But in health insurance, this may lead to fragmentation and market failure.

That’s because as insurers scramble for ideal customers – those least likely to get sick – they drive higher-risk people away by charging them higher premiums and making them foot a bigger share of their medical bills. Unfortunately, the latter (people often with preexisting conditions and requiring long-term treatment) really need medical care and the insurance coverage required to get it.

Because of this, all but the largest of the association health plans that the executive order is supposed to encourage still will most likely exclude high-risk individuals and employers, just as they have in the past, as health law expert Tim Jost predicts.

How will the vulnerable get health care?

the rich asshole said that his executive order will help “millions and millions of people.” But I believe it is more likely to drive coverage for many out of reach while benefiting the Americans whose insurance needs are relatively minimal.

One could argue that the government should never have tried to force healthier people to pay so much more for coverage to make it affordable for everyone else. Yet the nation needs a mechanism to help Americans with chronic and preexisting conditions pay for the medical care they need.

Establishing high-risk pools is one way to make this work, and they definitely can help as long as there is funding available. Unfortunately, most attempts to handle high-risk individuals this way have run out of money and left vulnerable patients high and dry. the rich asshole’s approach does nothing to deal with this.

Any solution that makes health insurance more affordable across the board will need to be comprehensive. I believe the rich asshole is instead embarking on a process that is both naïve and piecemeal based on wishful thinking regarding the power of markets to resolve all the problems with this difficult sector.

During his signing ceremony, he promised that the policies established by the order would “cost the government virtually nothing.” If that proves true, it is likely that we will receive exactly what we pay for.

J.B. Silvers, Professor of Health Finance, Weatherhead School of Management & School of Medicine, Case Western Reserve University

This article was originally published on The Conversation. Read the original article

White House desperately tries to fix the rich asshole’s widely-mocked claim he met with ‘president of the Virgin Islands’

some rich asshole (Screenshot/YouTube)

DON'T MISS STORIES. FOLLOW RAW STORY!

During his speech at the Values Voters summit on Friday, President some rich asshole told the crowd that he recently met with the “president of the Virgin Islands.”

This claim was quick to draw ridicule because the Virgin Islands are an American territory — which means the rich asshole himself is actually the president of the Virgin Islands.

As noted by CNN’s Kaitlan Collins, the official White House transcript of the president’s remarks actually crosses out the word “president” and replaces it with the correct title: “governor of the Virgin Islands.”

{kind=link}

the rich asshole lashes out at Puerto Rico as House passes $36.5 billion aid package

Ken Thomas and Andrew TaylorAssociated Press

President some rich asshole lashed out at hurricane-devastated Puerto Rico on Thursday, insisting in tweets that the federal government can't keep sending help "forever" and suggesting the U.S. territory was to blame for its financial struggles.

His broadsides triggered an outcry from Democrats in Washington and officials on the island, which has been reeling since Hurricane Maria struck three weeks ago, leaving death and destruction in an unparalleled humanitarian crisis.

San Juan Mayor Carmen Yulin Cruz, with whom the rich asshole has had a running war of words, tweeted that the president's comments were "unbecoming" to a commander in chief and "seem more to come from a 'Hater in Chief.'"

"Mr. President, you seem to want to disregard the moral imperative that your administration has been unable to fulfill," the mayor said in a statement.

The debate played out as the House passed, on a sweeping 353-69 vote, a $36.5 billion disaster aid package that includes assistance for Puerto Rico's financially-strapped government. House Speaker Paul Ryan, R-Wis., said the government needs to ensure that Puerto Rico can "begin to stand on its own two feet" and said the U.S. has "got to do more to help Puerto Rico rebuild its own economy."

Forty-five deaths in Puerto Rico have been blamed on Maria, about 85 percent of Puerto Rico residents still lack electricity and the government says it hopes to have electricity restored completely by March.

Both the rich asshole and Vice President Mike Pence visited the island last week to reaffirm the U.S. commitment to the island's recovery. But the rich asshole's tweets Thursday raised questions about whether the U.S. would remain there for the long haul. He tweeted, "We cannot keep FEMA, the Military & the First Responders, who have been amazing (under the most difficult circumstances) in P.R. forever!"

In a series of tweets, the president added, "electric and all infrastructure was disaster before hurricanes." He blamed Puerto Rico for its looming financial crisis and "a total lack of accountability."

The tweets conflicted with the rich asshole's past statements on Puerto Rico. During an event last week honoring the heritage of Hispanics, for example, the president said, "We will be there all the time to help Puerto Rico recover, restore, rebuild."

White House chief of staff John Kelly, speaking to reporters, said the military and other emergency responders were trying very hard to "work themselves out of a job." Reassuring the island, Kelly said the U.S. will "stand with those American citizens in Puerto Rico until the job is done."

At the Pentagon, Lt. Gen. Kenneth F. McKenzie Jr. told reporters "there's still plenty of work to be done" by the military troops in Puerto Rico. He said there was no current plan to withdraw troops who are supporting FEMA's recovery efforts. McKenzie, director of the military's Joint Staff, said it will be up to FEMA and other civilian agencies to decide when the military is no longer needed there.

Democrats said the rich asshole's tweets were deplorable, given that the 3 million-plus U.S. citizens on Puerto Rico are confronting the kind of hardships that would draw howls of outrage if they affected a state. One-third of the island lacks clean running water and just 8 percent of its roads are passable, according to government statistics.

"It is shameful that President the rich asshole is threatening to abandon these Americans when they most need the federal government's help," said Maryland Rep. Steny Hoyer, the second-ranking House Democrat.

After years of economic challenges, Puerto Rico was already in the process of restructuring much of its $74 billion in debt before the hurricane struck. The financial situation is more complicated than the rich asshole's tweets suggest.

Puerto Rico lost population and jobs after Congress eliminated special tax breaks in 2006, making it more difficult to repay its debts. Yet lenders continued to extend credit to Puerto Rico despite its economic struggles, while pension costs strained Puerto Rico's government and its infrastructure deteriorated.

The legislative aid package totals $36.5 billion and sticks close to a White House request. For now, it ignores huge demands from the powerful Florida and Texas delegations, which together pressed for some $40 billion more.

A steady series of disasters could put 2017 on track to rival Hurricane Katrina and other 2005 storms as the most costly set of disasters ever. Katrina required about $110 billion in emergency appropriations.

The bill combines $18.7 billion for the Federal Emergency Management Agency with $16 billion to permit the financially troubled federal flood insurance program pay an influx of Harvey-related claims. An additional $577 million would pay for western firefighting efforts.

Up to $5 billion of the FEMA money could be used to help local governments remain functional as they endure unsustainable cash shortfalls in the aftermath of Maria, which has choked off revenues and strained resources.

Ryan, the House speaker, planned to visit Puerto Rico on Friday. He has promised that the island will get what it needs.